How to get a housing loan even if you're not earning enough.

Dreaming of buying a home but worried your income is too low to qualify? The good news: you can. Many Filipinos assume they're not eligible because they don't earn a high salary — but that's often not the case. Plenty of lenders work with first-time and modest-income buyers. Here's how to give yourself the best possible chance of getting approved.

Are you dreaming of buying a home? Are you curious about how to get a housing loan — and wondering whether it's even possible to qualify if you don't earn a high income? The honest answer is yes, you can. Many people believe they aren't eligible for a housing loan simply because their salary isn't high enough. But this isn't always the case. Many lenders are willing to work with would-be homeowners even when their income is lower than average.

So whether you're just starting out in your career or you've hit a few financial bumps along the way, keep reading. Below are the practical steps that give you the best chance of getting a housing loan approved in the Philippines — and how a mortgage broker like Nook can do the hard part for you, for free.

Four things that move the needle on approval.

1. Analyse your credit score

When you're looking for a housing loan, it's essential to check your credit score and make sure this important financial rating is in good shape. A strong score can be the difference between an approval and a rejection when you apply to banks or other lending institutions — so don't leave it to chance. You can assess your credit standing before you apply. If your score isn't where you'd like it to be, you can take steps to improve it: make all your payments on time (rent, utilities, car payments and the like), and keep your credit card balances low.

2. Have a down payment saved up

If you're serious about buying a home, start saving for a down payment as early as you can — or look into new properties where the developer lets you pay the down payment on an instalment basis. A down payment is the upfront money you put towards the purchase; typically, lenders will want you to have around 20% of the purchase price saved before they approve your loan. Saving that much can feel intimidating, but there are simple ways to get there. Set up a budget and automate a monthly transfer into savings so a fixed amount is set aside before you spend on anything else. And trim unnecessary expenses — eating out, subscriptions and impulse buys — to free up more for your deposit.

3. Get help from a housing loan expert

If you're struggling to pull together a down payment, or you simply don't know where to begin, get expert help. Book a free housing loan consultation call with a Nook expert. They can tell you how much you may be able to borrow and what kind of rate to expect based on your financial situation. It's important to compare housing loan rates from multiple lenders before you decide — and that's exactly what Nook does, comparing 20+ banks for you. You can also use Nook's online loan calculators to estimate your monthly repayments, or have your consultant work them out with you. A Nook expert can even help you structure the loan to improve your chance of approval — for example, by adding a co-borrower.

4. Don't be hesitant to seek help

If you're still feeling stressed or confused, don't worry — most people feel overwhelmed at the thought of going through the housing loan application alone, or of trusting a real estate broker or property developer with such a major financial decision. A mortgage broker like Nook is staffed by housing loan professionals whose entire job is to find you the right loan, from the right bank, for your situation. And here's the part that surprises most people: because the banks pay Nook a commission once your loan is released, it costs you nothing.

Wrap up

So there you have it. These are some of the most effective ways to get a housing loan even if you think you're not earning enough money. With a little planning and effort, homeownership can be within reach — so don't give up on your dream just yet. And remember: Nook is here to help, completely free.

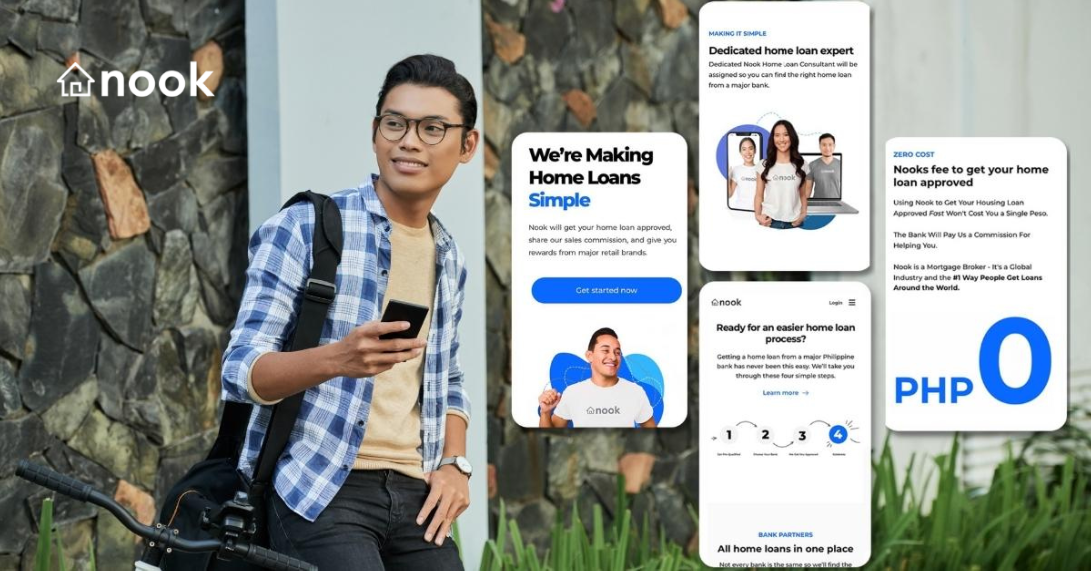

A dedicated expert does the whole application for you.

Nook is the Philippines' original and award-winning mortgage broker. You don't fill in bank forms or line up at branches — your consultant handles it all. Every application comes with four things built in.

Dedicated Loan Expert

A dedicated Nook loan consultant is assigned to you so you can find the right loan from a major bank effortlessly.

Chat Support Whenever You Need It

Support from our team is always available if you ever have a question, concern, or just want to chat.

Automated Loan Alerts & Updates

Constant progress updates via text and email alerts, so you're never left wondering what's happening.

Bank Communication Handled For You

Nook takes care of all the back-and-forth with the bank, so you don't have to.

One application, or twenty banks working in your favour.

Applying to a single bank and hoping you meet its criteria is the slow, old-fashioned way — and the riskiest if your income is modest. Nook gives you more lender choice, and the maximum chance of approval.

✦ With Nook

- ✓ 20+ lenders compared, so you're matched to the bank most likely to approve you

- ✓ The entire application done for you — and it's free

- ✓ Help structuring the loan, including adding a co-borrower

- ✓ A dedicated expert and progress updates at every step

Do it yourself

- ✕ One bank, one set of criteria, one chance of approval

- ✕ Forms and paperwork to complete on your own

- ✕ Time wasted lining up and following up at branches

- ✕ Little guidance if your income is on the lower side

Getting a housing loan on a lower income.

Can I get a housing loan in the Philippines if I have a low income?

Yes — a lower-than-average income doesn't automatically disqualify you. Banks look at the whole picture: your credit history, how stable your income is, your existing debts, and the size of your down payment. Many lenders are willing to work with first-time and modest-income buyers. Because each bank weighs these factors differently, the smartest move is to compare lenders rather than apply to just one. Nook compares 20+ banks and matches you to the one most likely to approve you — at the sharpest rate, and completely free.

How much income do I need to qualify for a home loan in the Philippines?

There's no single fixed figure — each bank sets its own minimum, and most assess whether your monthly loan repayment fits comfortably within your income alongside your other obligations. Rather than guessing whether you earn enough for one particular bank, get pre-qualified with Nook in about 3 minutes. You'll see which lenders you're actually eligible to borrow from based on your real situation, with no obligation and nothing to pay.

Can I add a co-borrower to help qualify for a housing loan?

Yes. Adding a co-borrower — such as a spouse, parent, sibling or child — combines both incomes, which can lift your borrowing power and improve your chance of approval if your income alone falls short. A Nook loan consultant can help you structure the application this way and match it to a bank that accepts co-borrowers, so you get the best possible result for your situation.

How can I improve my chances of getting a home loan approved?

Check and improve your credit score by paying bills, rent and card balances on time and keeping balances low. Save a larger down payment — many banks look for around 20% of the purchase price, though some developers let you pay it in instalments. Reduce existing debts, and consider adding a co-borrower. Finally, apply through a broker like Nook that compares 20+ banks, so you're matched to the lender most likely to say yes rather than gambling on one application.

How much down payment do I need for a housing loan in the Philippines?

Lenders commonly look for a down payment of around 20% of the property's purchase price, though this varies by bank and property type. A bigger down payment lowers the amount you need to borrow and can strengthen your application. If saving the full amount feels daunting, some developers let you pay the down payment in instalments, and a Nook consultant can point you to loan structures that suit a smaller deposit.

Does it cost anything to get help from Nook with my housing loan?

No — Nook is 100% free for borrowers. The banks pay Nook a commission once your loan is released, so you never pay a fee. You get a dedicated loan consultant who compares 20+ banks and handles your entire application for you — the forms, the paperwork and the follow-ups with the bank — at no cost. You can also book a free housing loan consultation call to talk through your options.

Not sure if you earn enough? Let's find out — free.

Pre-qualify online in about 3 minutes and see which of 20+ banks you're eligible to borrow from. Or chat to a live Nook agent for free advice on getting approved. Either way, Nook does the entire application for you, at no cost.

Check my rate →