How to avoid home loan repayment stress.

As the cost of living keeps rising, more people find their monthly repayments becoming a heavy burden. Here's what home loan stress really means, how to spot the warning signs, and the practical steps you can take to avoid it — or ease it if you're already feeling the pinch.

Can refinancing my home loan reduce repayment stress?

Yes. If you're on an older, higher rate, refinancing to a sharper rate lowers your monthly repayment and eases the pressure on your budget. You can also extend the term to reduce the payment, though that increases total interest over time. Nook compares 20+ banks, finds you a better home loan and manages the entire takeout from your current lender — for free, because the bank pays Nook a commission, not you.

As the cost of living continues to rise, more people are finding themselves suffering from monthly loan repayment stress. It's a quiet, common problem — and one that's far easier to avoid than to escape once it takes hold. In this guide we'll explain what home loan stress actually means, how to recognise it, and the practical things you can do to keep your repayments comfortable.

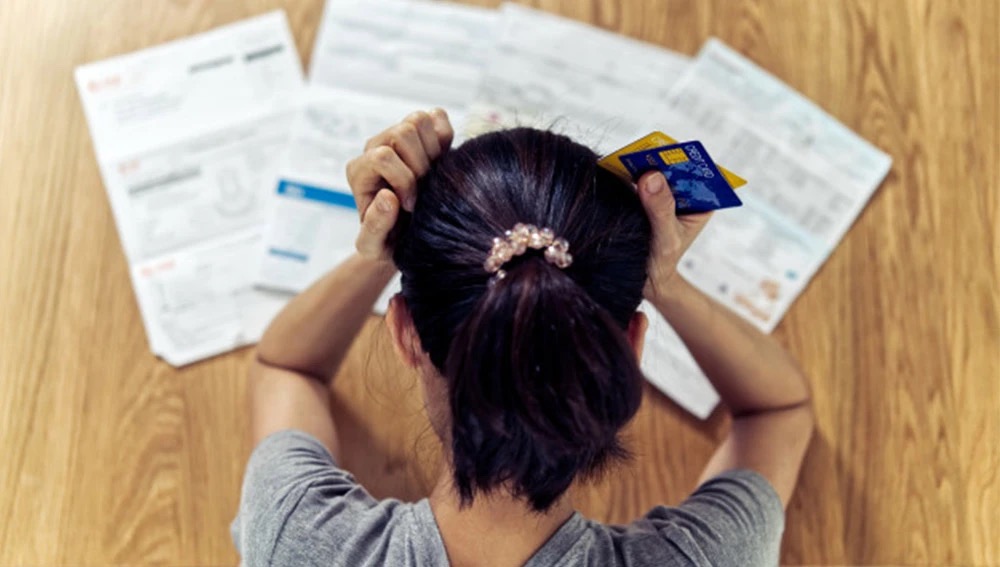

What is home loan repayment stress?

Loan stress is the feeling that creeps in when your monthly loan repayments are so high you have trouble paying your other bills. The common threshold is when mortgage repayments exceed 30% of your household income. Beyond that point, the loan starts crowding out everything else — and the strain is real. It's a painful, stressful feeling that damages families and is a common cause of relationship breakdown.

People usually fall into this pressure for one of a few reasons. Most often, they've taken on a bigger loan commitment than they comfortably should have. Sometimes it's a sudden change — losing a job, an illness, or a major unexpected expense. And sometimes new borrowers start with good intentions and a fresh budget, but find it too hard to actually trim the lifestyle they've grown used to. Whatever the cause, the fix starts with understanding the numbers before you commit.

Take the home loan stress test

There's no single definition of home loan stress that fits everyone. But if you answer "yes" to most of these questions, it's a good sign you're feeling the home loan pinch:

- Are you having trouble paying your electricity and other utility bills?

- Does more than 30% of your salary go towards your home loan repayments?

- Are you expecting a baby soon and worried about how you'll cover the costs of raising a child?

- Are you planning a wedding and equally worried about how you'll fund it?

- Are you concerned about how you'll pay for a new car or other large purchases?

- Are you having trouble paying off a credit card or other personal loan?

How can I avoid loan stress?

The easiest way to avoid the dreadful feeling of home loan stress is to buy a home that sits comfortably within your current budget. That headroom lets you build savings that can carry you through any unexpected financial emergency. Lending guidelines and bank policies are designed to stop you over-stretching — but you have to do your part too. Always provide honest, detailed information about your income and living expenses, and never let anyone helping with your application convince you to falsify documents. It can leave a black mark in bank databases and almost always leads to far greater pain down the track. Beyond that, three habits make the biggest difference:

- Use a budgeting tool. Most people under-estimate their expenses. Track everything in a spreadsheet or budgeting app so you get a clear, honest picture of your finances — and a realistic sense of the monthly repayment you can actually afford.

- Save cash regularly. Set up automatic deposits into a savings account and leave them there for genuine emergencies only — a sudden job loss or illness. This buffer is what stops a rough month from turning into a defaulted loan.

- Make extra repayments when you can. Whenever it's affordable — and provided your loan doesn't penalise it — pay a little more than the minimum. This reduces your principal and, with it, all the future interest you'd otherwise pay.

What should you do if you're feeling loan stress now?

If you're already in it, the situation can feel horrible — but there are real ways to reduce the pressure. The worst thing you can do is stay silent and miss a repayment.

- Talk to your bank. Have an honest conversation first. You may be able to consolidate loans, and depending on your situation some banks can reconfigure your monthly repayments or offer a short "holiday period" without repayments to help you get back on track. If the stress is temporary, even a better budget can be enough.

- Eliminate unnecessary spending. When you're used to a certain standard of living, cuts are hard — but missing a mortgage repayment is far worse. Trim back on restaurant and take-away meals, bring lunch to work, hold off on new clothes, and pause non-essential luxuries like streaming subscriptions or cable until you're steady again.

- Consider refinancing to a lower rate. If you're paying an old, high rate, moving to a sharper one cuts your monthly repayment directly. Nook compares 20+ banks, finds you a better home loan, and handles the entire takeout from your current lender — for free.

We're making home loans simple

The single biggest protection against repayment stress is borrowing the right amount, from the right lender, at the right rate — from the very start. That's exactly what Nook does. As the Philippines' original and award-winning mortgage broker, Nook compares 20+ banks and matches you to the lender most likely to approve you at the sharpest rate. You can pre-qualify in about three minutes and see a repayment that genuinely fits your budget before you commit to anything.

And because Nook does the entire application for you — the bank forms, the paperwork, the follow-ups — there are no branch queues and no piles of forms to wrestle alone. Best of all, it's 100% free: banks pay Nook a commission once your loan is released, not you. Whether you're buying your first home or refinancing to ease the pressure on an existing loan, Nook gives you the choice and the support to keep your repayments comfortable.

Questions about keeping your home loan comfortable.

What is considered home loan stress in the Philippines?

As a rule of thumb, you're in home loan stress when your monthly mortgage repayments exceed about 30% of your household income. At that point the loan starts crowding out other essentials — utilities, groceries, transport — and it becomes hard to set anything aside for emergencies. Borrowing within a comfortable share of your income, and pre-qualifying before you commit, is the simplest way to stay below that threshold.

How much of my income should go to a housing loan repayment?

Aim to keep your home loan repayment under roughly 30% of your gross household income, leaving room for utilities, food, transport and savings. Banks in the Philippines also apply their own debt-to-income limits when assessing you. Nook compares 20+ lenders and pre-qualifies you in about 3 minutes so you can see a repayment that actually fits your budget before you apply — completely free.

What should I do if I'm already struggling with my repayments?

Act early. Talk to your bank first — many lenders can restructure your repayments, consolidate loans, or offer a short payment holiday to help you get back on track. At the same time, cut non-essential spending such as dining out, subscriptions and impulse purchases before you ever miss a repayment, since a missed payment has far heavier consequences. Refinancing to a lower rate can also reduce the monthly amount, and Nook handles that takeout for you for free.

Can refinancing my home loan reduce repayment stress?

Yes. If you're on an older, higher rate, refinancing to a sharper rate lowers your monthly repayment and eases the pressure on your budget. You can also extend the term to reduce the payment, though that increases total interest over time. Nook compares 20+ banks, finds you a better home loan and manages the entire takeout from your current lender — for free, because the bank pays Nook a commission, not you.

How can I lower my monthly home loan repayments?

There are a few levers: borrow within your budget from the start, refinance to a lower interest rate, or lengthen your loan term to spread the cost (at the price of more total interest). On the other side, making extra repayments when you can afford it shrinks your principal and your future interest. The best first step is to compare lenders — Nook checks 20+ banks and lets you pre-qualify in 3 minutes to find the most affordable, best-fit loan, free of charge.

Does making extra home loan repayments help avoid stress?

It can — provided your loan doesn't penalise early or extra payments. Paying a little more than the minimum when you can afford it reduces your outstanding principal, which lowers the interest you pay over the life of the loan and shortens the term. Pair that with an emergency savings buffer so you never have to choose between a repayment and an unexpected bill. Choosing a flexible loan from the right lender makes this far easier, which is exactly what Nook helps you find.

Borrow comfortably from the start.

Pre-qualify in 3 minutes and see a repayment that fits your budget — or refinance to a lower rate to ease the pressure on an existing loan. Nook compares 20+ banks and does the entire application for you. It's 100% free.

Check my rate →